But even if an expense is ordinary and necessary, you may still not be able to deduct all of it on your taxes. Just because you do is my company required to file an incurred cost submission most of your work from your dining room table doesn’t mean that you can deduct your entire monthly rent. Luckily, the IRS has put together a comprehensive guide on business deductions that you can consult if you’re ever unsure about a deduction.

These business activities are recorded based on the company’s accounting principles and supporting documentation. Since good record keeping relies on accurate expense tracking, it’s important to monitor all transactions, keep receipts, and watch business credit card activity. Many bookkeeping software options automate the tracking process to eliminate errors.

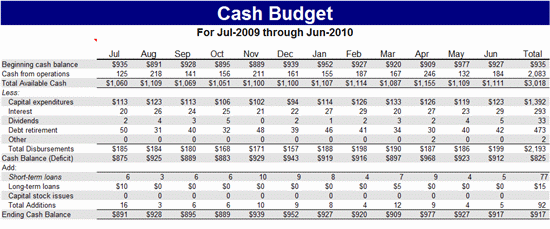

Balance your books

Many of the operations are automated in the software, making it easy to get accurate debits and credits entered. When an effective bookkeeping system is in place, businesses have the knowledge and information that allows them to make the best financial decisions. Tasks, such as establishing a budget, planning for the next fiscal year and preparing for tax time, are easier when financial records are accurate. At tax time, the burden is on you to show the validity of all of your expenses, so keeping supporting documents for your financial data like receipts and records is crucial. Mixing together personal and business expenses in the same account can also result in unnecessary stress when you need to file taxes or do your bookkeeping.

Double-entry bookkeeping records all transactions twice, usually a debit and a credit entry. Typically, double-entry bookkeeping uses accrual accounting for liabilities, equities, independent contractor agreement for accountants and bookkeepers assets, expenses and revenue. Whether it’s updating your books or keeping in contact with your tax adviser, maintain your business’s financial records and expenses throughout the year. That way, you can be well prepared when it’s time to file taxes with the IRS.

- Bookkeeping serves as more of a preliminary function through the straightforward recording and organizing of financial information.

- Finally, you’ll want to decide how all receipts and documents will be stored.

- Every transaction you make needs to be categorized when it’s entered in your books.

- Do you have more questions about the bookkeeping process for small businesses?

- The specific amount of an emergency fund may depend on the size, scope, and operational costs of a given business.

What Is Financial Bookkeeping?

No matter what system you implement, incorporate a practice of reconciliations, by comparing the stale dated checks numbers in your system to the source records, like bank statements, receipts, and invoices. This habit improves communication, boosts transparency with your bookkeeping team, and promotes longevity and compliance. It might feel daunting at first, but the sooner you get a handle on this important step, the sooner you’ll feel secure in your business’s finances. Remember that the basic goals of bookkeeping are to track your expenses and profits, and to ensure you collect all necessary information for tax filing. Business accounting software and modern technology make it easier than ever to balance the books. A platform like FreshBooks, specifically designed for small business owners, can be transformational.

Track expenses

It could mean a business expense gets lost in your personal account and you miss out on an important deduction. If you need to borrow money from someone other than friends and family, you’ll need to have your books together. Doing so lets you produce financial statements, which are often a prerequisite for getting a business loan, a line of credit from a bank, or seed investment.

There are several standard methods of bookkeeping, including the single-entry and double-entry bookkeeping systems. While these may be viewed as “real” bookkeeping, any process for recording financial transactions is a bookkeeping process. The bookkeeping transactions can be recorded by hand in a journal or using a spreadsheet program like Microsoft Excel.

The equity accounts include all the claims the owners have against the company. The business owner has an investment, and it may be the only investment in the firm. In this day and age, the providers you contract with don’t need to be in the same city, state or even time zone as you. Remote work has expanded across nearly every field, including bookkeeping. If you find someone who is a good fit for your business needs, it doesn’t matter if they are in California while you work from New York. You’ll want to create a contract that outlines details, such as deadlines, rates and expectations so that everyone is on the same page.

Deixe uma resposta

Want to join the discussion?Feel free to contribute!